Watching the Bond Market First

the bond market has long acted as an early signal for broader financial markets. While stocks often grab headlines, bonds quietly reflect shifts in growth, inflation, and risk appetite. At key moments, those shifts show up in bonds first, then work their way into equities. That is why we continue to watch the bond market closely.

Right now, U.S. Treasury futures have faced pressure, which pushed yields higher earlier in the cycle. History shows that fast moves in yields tend to matter for stocks. Higher yields change how investors discount future earnings. They also reset how attractive risk-free assets look compared to stocks. When this adjustment happens quickly, equity markets often react with more volatility.

The recent activity in the 10-year Treasury is not just about rates. Global factors are playing a role. Geopolitical tension has returned to the center of market thinking. Trade threats, shifting alliances, and political uncertainty have made some investors less willing to hold U.S. assets. This has led to talk of a “sell America” trade in certain circles. When demand for Treasuries softens, bond prices fall and yields rise.

Inflation expectations are another key driver. Even with discussions around possible rate cuts later on, many investors remain cautious. Strong economic data and large government borrowing needs have raised questions about how quickly inflation will cool. As a result, bond investors are asking for higher yields to hold government debt. This tells us that confidence, while not broken, is being tested.

Why does this matter for equities? Rising yields increase borrowing costs for companies and consumers. They also give investors another option for returns. When bonds pay more, stocks must justify their risk. This can put pressure on valuations, especially in sectors that rely heavily on cheap financing. It does not mean stocks must fall, but it often leads to sharper rotations and narrower leadership.

This is where diversification becomes critical. At the Trading Desk, we believe portfolios should not depend on a single asset class. Markets move in cycles, and leadership changes over time. A diversified mix helps smooth returns when signals from one market turn less supportive.

Our model portfolio reflects this view. We look to equities, at 40%, for long-term growth. Fixed income, at 25%, plays a role in income and stability. Commodities and real assets, at 20%, help address inflation risk and diversification. Cash, at 10%, provides flexibility and the ability to respond when opportunities appear.

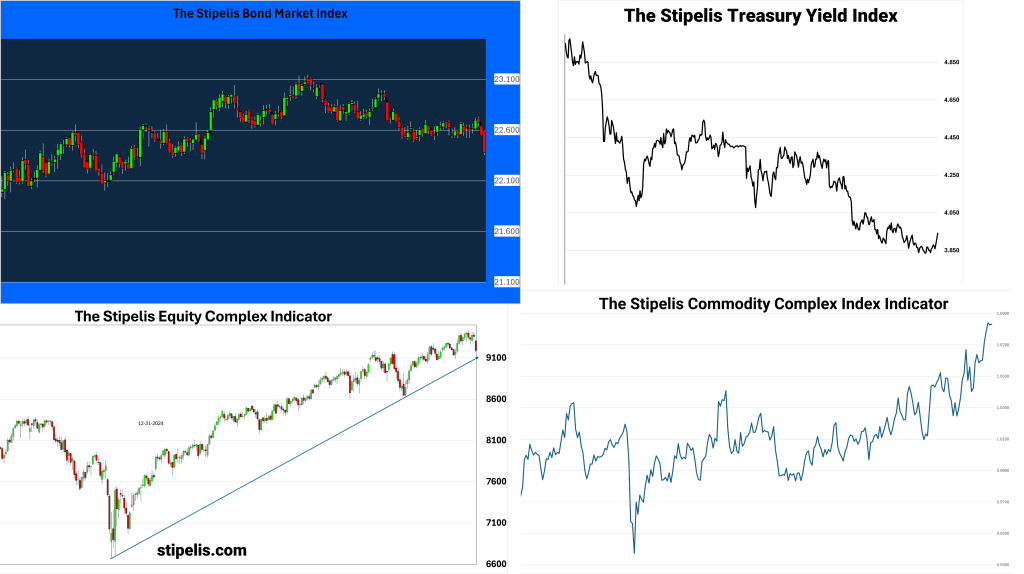

Looking across the current charts, the message is mixed but constructive. The Stipelis Bond Market Index is holding near the upper end of its range, showing steady demand on pullbacks. Treasury yields have eased more recently, suggesting the market is stepping back from earlier rate stress. Equities remain in an uptrend, supported by lower yields. Commodities are also gaining traction, pointing to uneven but ongoing growth.

The bond market is not forecasting outcomes with certainty. What it offers is information. Right now, that information points to caution, selective risk-taking, and the importance of balance. Investors who respect these signals may be better positioned as markets adjust and leadership evolves.

The Trading Desk at Stipelis